Lease end has a way of sneaking up on you. One week you’re fine, the next you’re staring at a deadline, a mileage number, and a pile of “maybe” choices that all sound expensive.

Here’s the good news: most lease-end decisions get easier when you stop thinking in terms of “What should I do?” and start with “What’s my car worth compared to my contract?” That’s the math part. The same framework applies whether you’re evaluating a Toyota lease buyout or any other brand’s end-of-lease option.

Then you add real life, your budget, your commute, and how much you like the car.

This guide gives you a simple framework for the four main options, return, buy, trade, or lease new, plus one pressure valve that buys time: a short lease extension.

With the global vehicle leasing market size expected to grow to over $1 trillion by 2033, with a CAGR of 6.78%, this is an industry you want to be able to navigate well.

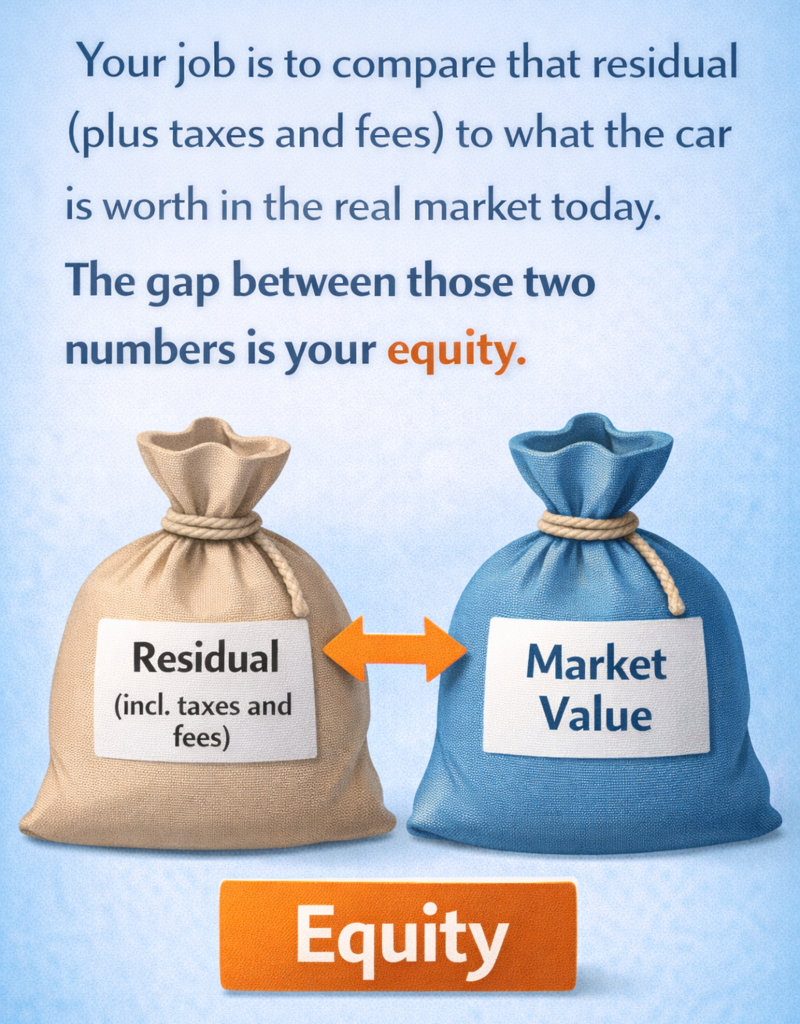

At lease end, you’re not guessing. Your contract already includes a price to buy the car. That number is the residual value, basically the bank’s pre-set “end price” for the vehicle.

Here’s a practical way to run it in 10 minutes:

You want offers that reflect what someone will actually pay, not a hopeful estimate.

Start with an online instant offer, then get a written appraisal from a local dealer. If you can, add one more quote from another dealer or used-car buyer.

Condition changes the number fast. Tires close to replacement, a cracked windshield, or a deep scrape can pull your offer down. A clean interior, both keys, and service records can push it up.

Lease-end math goes sideways when you forget the add-ons. Before you choose a path, list the costs that could show up on your final bill. Looking at large expenses through a structured lens helps, whether you’re pricing a vehicle transition or comparing projections like how much long-term care costs..

Common ones include:

Once you know whether you have positive or negative equity, the best lease-end choice usually becomes obvious. It’s less about preference and more about protecting your money.

In early 2026, used car prices have shown mild upward movement at wholesale auctions (about 2.4% to start the year), and many popular gas and hybrid models have held value well. That can mean more lease-end positive equity than people expect.

EVs are a different story; more off-lease EV supply has pushed many used EV prices down, so the contract buyout is more likely to be higher than market value on some EV leases.

Here’s how the main options tend to line up.

Pros:

Watch-outs:

Best for: cars with negative equity, high miles, or issues you don’t want to fix.

If you have positive equity, you should think twice before returning the car. You might be handing value back to the bank.

Buying it out (then keeping it):

Buying it out (then selling it)

Trading it in (often into another lease or purchase)

Best for: shoppers who want a different vehicle and want the dealer to handle the swap.