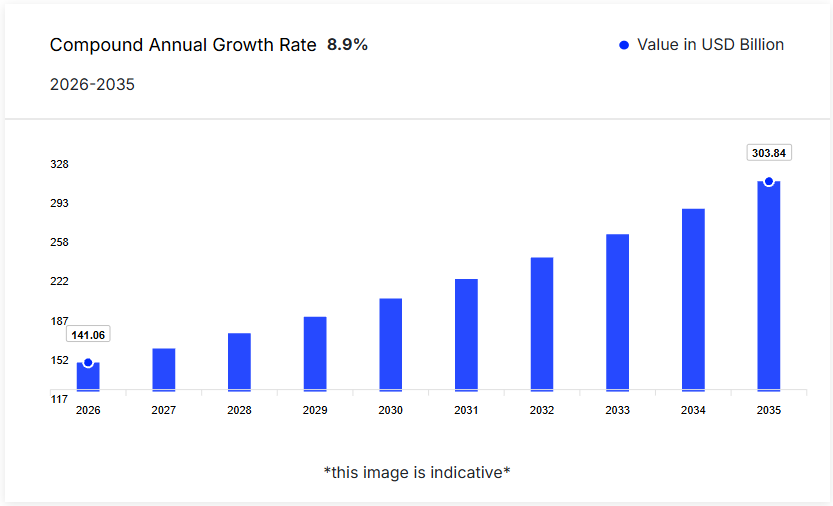

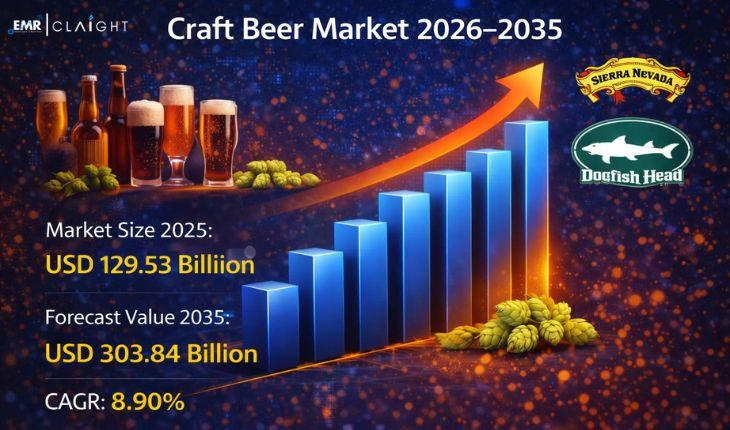

According to Expert Market Research, the craft beer market size reached a value of USD 129.53 billion in 2025 and is expected to grow at a CAGR of 8.90% during 2026-2035, reaching USD 303.84 billion by 2035. Market expansion is being supported by changing consumer preferences, particularly among younger demographics, who are actively seeking differentiated flavour profiles, small-batch positioning, and authentic brand stories. Craft breweries are responding with experimental styles and limited releases, while improvements in retail availability and e-commerce distribution are broadening consumer access to niche offerings.

A key market characteristic is the continued shift from mainstream beers toward premium and specialty categories. This is reinforced by increasing willingness to pay for perceived quality, local provenance, and product variety. At the same time, the competitive landscape is becoming more complex as established brewers expand craft portfolios and independent players scale distribution through off-trade and online channels.

Analysts note: Category growth is increasingly driven by portfolio differentiation and availability across modern retail and digital purchase journeys, rather than taproom-only consumption.

Craft beer is typically positioned around smaller-scale production, style experimentation, and brand identity built on local or niche appeal. The category includes a wide range of styles, from lagers and pilsners to ales and specialty beers featuring unique hops, adjunct ingredients, barrel ageing, or seasonal variants. This diversity supports repeat purchases and discovery-led consumption, particularly among consumers looking to move beyond standard mainstream offerings.

Download a Free Sample Report With TOC

The market is also evolving in how craft is accessed. Traditional on-trade influence remains important for discovery, but off-trade and digital channels increasingly shape volume growth, particularly where home consumption trends and convenience-driven purchase behaviour are strengthening.

Rising Demand for Unique and Innovative Flavours

A sustained driver for craft beer demand is the preference for distinct taste experiences. Consumers are actively exploring new styles, flavours, and limited releases, encouraging brewers to increase experimental product pipelines. Brands such as Dogfish Head and Sierra Nevada are widely recognised for experimental brews and innovation-led portfolio strategies, illustrating how novelty can support market momentum.

Premiumisation and “Better-For-Experience” Consumption

Craft beer continues to benefit from premiumisation, where consumers prioritise quality, freshness, and differentiated taste over higher volumes of standard beer. This supports higher average selling prices, wider margins for differentiated styles, and increased attention to packaging, branding, and product storytelling at the point of sale.

Expansion of E-commerce and Digital Alcohol Delivery

E-commerce has improved access to a broader variety of craft options, enabling consumers to discover and purchase niche brands beyond local availability. Platforms such as Drizly (where available) have contributed to category visibility by aggregating craft selections and supporting search-driven purchasing. This channel is particularly relevant for limited releases, variety packs, and seasonal rotations.

Broader Off-trade Distribution and Retail Shelf Visibility

Off-trade distribution through supermarkets, hypermarkets, specialty liquor stores, and convenience retail is widening craft beer reach. Retail shelf presence increases trial potential, supports repeat purchasing, and shifts craft beer from occasional consumption to routine household buying behaviour in many markets.

Portfolio Expansion Through Specialty Beers

Specialty beers are gaining attention through seasonal launches, experimental ingredient combinations, and limited-edition positioning. These products help breweries maintain consumer interest, support higher price points, and reduce dependency on a narrow core range.

Brand Collaboration and Limited-Release Strategies

Collaborations between breweries, cross-style experimentation, and rotating product calendars are strengthening discovery-led demand. This trend supports social sharing, on-trade visibility, and differentiated retail assortments.

Omnichannel Purchase Journeys

Consumer buying is increasingly split across on-trade discovery, off-trade replenishment, and online exploration. Breweries with distribution breadth and consistent product availability across channels are better positioned to scale.

By Type

By Distribution Channel

North America: Mature and high-value market supported by strong consumer demand and advanced infrastructure.

Europe: Stable growth driven by established industries and integrated trade networks.

Asia Pacific: Fastest-growing region fueled by industrial expansion and rising consumption.

Latin America: Emerging market supported by improving infrastructure and expanding regional trade.

Middle East and Africa: Developing region benefiting from economic diversification and infrastructure investments.

The market includes established craft brewers and scales players with multi-brand portfolios. Competitive advantage is increasingly linked to distribution reach, innovation cadence, and brand distinctiveness.

Companies Covered

Input Cost Volatility and Supply Constraints

Craft beer production can be exposed to volatility in key inputs such as malt, hops, glass/aluminium packaging, and logistics. Cost pressures can affect pricing strategies and margins, particularly for smaller brewers.

Distribution Gatekeeping and Shelf Competition

Retail shelf space is competitive, and craft brands must continuously justify placement through velocity, differentiation, and promotional support. This can disadvantage smaller players with limited scale.

Regulatory and Compliance Complexity

Alcohol regulation varies widely across markets, affecting advertising, direct shipping, and online sales. Compliance requirements can limit expansion strategies for cross-border and e-commerce growth.

Brand Dilution and “Craft-Washing” Concerns

As large beer groups expand craft-style offerings, consumer perception around authenticity can become a market friction point. Independent brewers may need stronger brand cues to protect differentiation.

The craft beer market is expected to maintain robust growth through 2035, supported by premiumisation, continued flavour innovation, and broader availability through off-trade and online channels. Breweries that sustain innovation pipelines, build scalable distribution, and remain relevant across changing consumption occasions are likely to strengthen competitive positioning over the forecast period.

What was the craft beer market value in 2025?

The craft beer market reached approximately USD 129.53 Billion in 2025, driven by rising demand for innovative and flavour-focused brews.

What is the expected growth rate of the craft beer market during 2026-2035?

The industry is projected to grow at a CAGR of 8.90% during the forecast period, supported by premiumisation and expanding e-commerce access.

What is the forecast value of the craft beer market by 2035?

By 2035, the market is expected to reach around USD 303.84 Billion, reflecting continued consumer interest in experimental and specialty craft offerings.

What is driving growth in the craft beer market?

Growth is driven by consumer preference for unique flavours, premium positioning, and wider access through retail and e-commerce channels.

Which craft beer types are gaining traction?

Ales and specialty beers are attracting demand due to innovation, variety, and limited-release strategies, while premium lagers are expanding appeal to wider audiences.

How is e-commerce influencing craft beer sales?

E-commerce improves access to broader assortments and discovery-led buying, particularly for consumers outside major brewery hubs and for seasonal or niche styles.

Expert Market Research is a global market intelligence and consulting platform by Claight delivering data-driven insights across commodities, chemicals, energy, and industrial markets. We design our research to support businesses, analysts, investors, and procurement teams in understanding price trends, supply-demand dynamics, competitive landscapes, gaining competitive intelligence, benchmarking best practices, and developing long-term market outlooks.

Our robust research methodologies, combined with validated primary and secondary data, ensure accuracy, consistency, and relevance. Our analysis is widely used not only for strategic planning, market-entry assessments, and sourcing decisions, but also for investment evaluation across international markets. Our strong emphasis on transparency, factual reporting, and regular data updates to reflect real-time market conditions always keeps you ahead of the curve.

To better serve regional and language-specific audiences, we also operate Informes de Expertos, our dedicated Spanish-language market research platform. Informes de Expertos is specifically designed for Spanish-speaking countries, providing localised market intelligence, pricing insights, and industry analysis aligned with regional business needs and search behaviour.

Procurement Resource is also a part of our integrated insights ecosystem. An AI-enabled platform focusing on price trends, cost structures, trade data, cost modeling and procurement intelligence for commodities and industrial inputs. It is designed to support buyers, sourcing professionals, and supply-chain teams with not just actionable pricing data but also procurement-focused insights, saving costs and giving you better visibility of what the future holds.

Together, these platforms form a unified market intelligence network built on accuracy, credibility, and practical relevance, serving global markets.

Company Name: Claight Corporation

Email: [email protected]

Toll Free Number: +1-415-325-5166 | +44-702-402-5790

Address: 30 North Gould Street, Sheridan, WY 82801, USA

Website: https://www.expertmarketresearch.com